For the past two years, employers have been tracking one of the most turbulent stretches in FLSA overtime rulemaking in decades. The Biden administration raised the salary threshold dramatically, courts struck it down, and then the current administration formally walked it back. And now, on top of the classification questions, a brand-new tax deduction for overtime pay has added a payroll reporting requirement that takes full effect in 2026. If you feel like you have been drinking from a firehose, you are not alone.

At Lift HCM, we work with small and mid-sized businesses every day to help them stay ahead of payroll and HR compliance changes. When the rules shift, our job is to translate what happened in federal court or the Federal Register into clear, practical steps your business can actually take. With more than 20 years of combined HR and payroll experience, our team has guided businesses through multiple rounds of FLSA rulemaking.

This article covers exactly what the DOL did in May 2026, what the current federal overtime salary threshold is, where employers still face real compliance exposure at the state level, what to do if your business already made changes for the now-rescinded 2024 rule, what the OBBBA overtime tax deduction means for your payroll reporting, what the penalties for misclassification look like, and what your complete action plan should be right now.

Key Terms Used in This Article

If you are new to FLSA overtime rules, these definitions will anchor everything that follows. If you are familiar with the basics, this section is a quick reference you can return to.

|

FLSA |

Fair Labor Standards Act. The federal law that establishes minimum wage, overtime pay, recordkeeping, and child labor standards. |

|

White-collar exemption |

FLSA exemption for executive, administrative, and professional employees who meet both a salary level test and a duties test. |

|

Salary level test |

The minimum weekly pay threshold ($684/week as of 2026) an employee must earn to qualify for a white-collar exemption. |

|

Duties test |

The requirement that an exempt employee's primary job duties match the legal definition of executive, administrative, professional, computer, or outside sales work. |

|

Salaried nonexempt |

A worker paid a fixed salary who is still legally entitled to overtime pay because they fail the salary level test or the duties test. |

|

Qualified overtime (OBBBA) |

The premium portion of FLSA overtime pay (the 'half' in time-and-a-half) that employees may deduct under the One Big Beautiful Bill Act for tax years 2025-2028. |

|

HCE |

Highly compensated employee. Eligible for a broader overtime exemption at a total annual compensation threshold of $107,432. |

Key Takeaways

The federal overtime salary threshold is $684 per week ($35,568 annually). The DOL announced a technical amendment on May 14, 2026, and published it in the Federal Register on May 15, 2026, formally confirming this as the operative standard for most white-collar exemptions.

The 2024 rule, which would have raised the threshold to $1,128 per week, had already been vacated by federal courts in late 2024. The May 2026 action makes that official in the Code of Federal Regulations.

Employers who raised salaries or reclassified employees in anticipation of the 2024 rule should evaluate whether to maintain or reverse those changes.

State overtime thresholds in California, Washington, Colorado, Maine, and New York are significantly higher than the federal level and continue to increase on annual schedules.

The OBBBA created a new federal overtime tax deduction for tax years 2025 through 2028. Starting with tax year 2026, employers must separately report qualified overtime on W-2s using Box 12 code 'TT' or face penalties. The deduction expires after 2028.

Overtime misclassification can result in up to three years of back wages, liquidated damages that double that amount, civil penalties, and in willful cases, criminal prosecution.

Table of Contents

-

What Is the Current Federal Overtime Salary Threshold in 2026?

-

What Does the OBBBA Overtime Tax Deduction Mean for Employers?

-

Frequently Asked Questions About the DOL Overtime Rule in 2026

-

Get the Right Overtime Compliance Foundation for Your Business

What Happened with the DOL Overtime Rule?

The short answer: On May 14, 2026, the DOL announced a technical amendment to formally rescind the Biden-era 2024 overtime rule. The amendment was published in the Federal Register on May 15, 2026, and took effect immediately. It restores the 2019 salary threshold of $684 per week as the operative federal standard and removes the 2024 rule language from the Code of Federal Regulations.

In April 2024, the Biden administration's DOL published a final rule raising the standard salary threshold for white-collar overtime exemptions in two phases. The first increase, to $844 per week, took effect July 1, 2024. A second increase, to $1,128 per week, was scheduled for January 1, 2025. The rule also included automatic triennial adjustments tied to wage data.

That plan did not survive contact with the courts. In November 2024, the U.S. District Court for the Eastern District of Texas vacated the entire 2024 rule, including the first increase that had already gone into effect. A separate federal court in the Northern District of Texas issued a similar ruling shortly after. Both decisions restored the 2019 threshold ($684 per week) as the operative standard. The DOL initially appealed both rulings to the U.S. Court of Appeals for the Fifth Circuit, but on May 5 and May 7, 2026, the agency dropped both appeals and the Fifth Circuit dismissed the cases.

On May 14, 2026, the DOL announced the technical amendment. It was published in the Federal Register on May 15, 2026, formally removing the vacated 2024 rule language from the Code of Federal Regulations and reinstating the 2019 regulation. The amendment took effect immediately. As the DOL put it, this action is a technical correction accounting for changes in the law that have already occurred.

What Is the Current Federal Overtime Salary Threshold in 2026?

The current federal overtime salary threshold is $684 per week ($35,568 annually) for most white-collar exemptions, and $107,432 annually for highly compensated employees. These thresholds were confirmed by the DOL's technical amendment published May 15, 2026, and there is no automatic adjustment mechanism currently in place.

Nondiscretionary Bonuses and Incentive Pay

Up to 10 percent of the standard salary level can be satisfied through nondiscretionary bonuses, incentives, and commissions, provided those amounts are paid annually or more frequently. Discretionary bonuses do not count.

Who is not subject to salary level and salary basis tests: Bona fide doctors, lawyers, teachers, and outside sales employees qualify for exemption based on duties alone. The salary level and salary basis tests do not apply to these categories.

Do the Duties Tests Still Apply?

Yes, the duties tests still apply and matter just as much as the salary level. An employee must meet three requirements to be exempt from overtime: the salary basis test, the salary level test ($684/week), and the applicable duties test. Meeting the salary threshold alone is not enough.

The salary basis test requires that the employee be paid a fixed, predetermined salary not subject to reduction based on the quality or quantity of work performed. The duties test requires that the employee's primary duties qualify them for executive, administrative, professional, computer, or outside sales exemption.

An employee who earns $700 per week but spends the majority of their time on routine, production-level tasks does not qualify for the administrative exemption, regardless of their title or job description.

One of the most common misconceptions: being paid a salary does not make an employee exempt. If a salaried employee earns less than $684 per week, they are nonexempt and entitled to overtime. If they earn above $684 per week but do not pass the duties test, they are also nonexempt. These are called salaried nonexempt employees, and they must have their hours tracked and receive overtime pay for any hours over 40 in a workweek, just like hourly employees. If you want a deeper look at how misclassification plays out in real dollars, read our guide, Are You Sure You’re Overtime Compliant? The Costly Truth About Employee Misclassification.

Common Duties Test Mistakes That Create Audit Exposure

-

Treating job titles as a proxy for exempt status. The title 'manager' does not confer an exemption. Actual duties do.

- Classifying supervisors as executive-exempt when they do not have genuine authority over hiring, firing, or significant personnel decisions.

- Applying the professional exemption broadly when it actually requires advanced knowledge in a recognized field of science or learning, typically acquired through specialized study.

- Conflating following established procedures or applying technical knowledge with exercising genuine discretion and independent judgment. These are not the same thing.

Review job descriptions and actual day-to-day duties any time an employee's role changes significantly. Documentation that does not reflect reality creates liability even when the salary level is correct.

What If My Business Already Made Changes for the 2024 Rule?

There is no legal requirement to undo changes made in anticipation of the 2024 rule. Salary increases can be maintained, and employees who were reclassified to nonexempt may be eligible for re-exemption if they meet the restored $684/week threshold and the applicable duties test. Any reversal should be evaluated on a role-by-role basis and documented carefully.

If You Raised Salaries

There is no legal requirement to reduce salaries that were increased in response to the 2024 rule. In many cases, maintaining the increase is the right call for employee morale and retention. However, employers who increased compensation significantly above $684 per week purely to preserve exempt status may want to evaluate whether the current salary, the duties test, and business needs still align.

If You Reclassified Employees from Exempt to Nonexempt

Employees who were reclassified to nonexempt status in anticipation of the 2024 rule may be eligible for re-exemption, provided they meet both the restored $684 per week salary threshold and the applicable duties test. Employers in California, New York, or other states with higher salary floors may have less flexibility depending on whether those employees also meet the relevant state salary level.

Before Making Any Changes, Document Your Reasoning

Reversing a reclassification carries risk if the duties test was always marginal or if the reclassification was communicated to the employee in a way that created expectations. Build a documented, role-by-role review before taking action. That documentation protects you in any future audit or dispute.

Where Is the Real Overtime Compliance Pressure in 2026?

State-level thresholds, not the federal floor, are where most employers face real overtime compliance risk in 2026. Five states (California, Washington, Colorado, Maine, and New York) maintain salary thresholds that significantly exceed the federal $684/week standard, and all five increase on an annual schedule. When state law is more protective than federal law, the state standard applies.

California

Exempt employees must earn at least twice the state minimum wage on a full-time basis, which means at least $1,352 per week ($70,304 annually) for most employees as of January 1, 2026. California also maintains a separate, higher threshold for computer software employees ($58.85/hr or $122,573.13/year) and is unique in imposing daily overtime: non-exempt employees earn overtime for any hours over eight in a single day, not just hours over 40 in a week.

Colorado

Colorado's Overtime and Minimum Pay Standards (COMPS) Order sets the weekly minimum at $1,111.23 per week ($57,783.96 annually) as of January 1, 2026. This updates annually. Confirm the current rate directly with the Colorado Division of Labor Standards and Statistics.

Maine

Maine's threshold is $871.16 per week ($45,300.32 annually) as of January 1, 2026, tied to the state minimum wage and updated annually. Employers in Portland and Rockland should check for any higher local minimum wage requirements. Maine also has a six-year statute of limitations for wage claims, longer than the federal standard, making correct classification particularly important for Maine employers.

New York

New York maintains salary thresholds that vary by region and increase annually. New York City and Long Island carry higher thresholds than the rest of the state. Verify the current applicable rate for each work location before making classification decisions.

Washington

Washington's threshold is $1,541.70 per week ($80,168.40 annually) for large employers as of January 1, 2026, tied to 1.75 times the state minimum wage. Small employers have a lower threshold. Computer professionals may alternatively be paid on an hourly basis at a minimum of $59.96 per hour. Confirm the current rate for your employer size with the Washington State Department of Labor and Industries.

Could the DOL Raise the Overtime Threshold Again?

Yes, future rulemaking is possible, but as of June 2026, no proposed rulemaking on overtime salary thresholds is pending. The DOL's May 2026 amendment explicitly preserves the agency's authority to conduct future rulemaking, but there is no automatic adjustment mechanism and no active proposal. Any future increase would require a formal notice-and-comment period, giving employers advance notice.

The U.S. Court of Appeals for the Fifth Circuit upheld the DOL's legal authority to set a salary floor for white-collar exemptions in September 2024, so the legal framework for a future increase remains intact.

-

No automatic adjustment mechanism is currently in place. The triennial adjustment provision was part of the 2024 rule and was rescinded along with it.

-

Any future increase would require new rulemaking, including a public notice and comment period. Employers would have advance notice before any new threshold takes effect.

-

The DOL's active rulemaking focus as of June 2026 is on joint employer standards, not overtime salary levels. A proposed rule issued April 22, 2026 seeks to clarify joint employer status under the FLSA, FMLA, and MSPA.

The businesses that managed the 2024 rule disruption with the least difficulty were the ones that already had a regular classification review process in place. Building that into your annual HR calendar now is the most resilient long-term approach.

What Does the OBBBA Overtime Tax Deduction Mean for Employers?

Starting with tax year 2026, employers must separately report qualified overtime compensation on W-2 forms using Box 12 code 'TT.' The One Big Beautiful Bill Act (OBBBA), passed July 4, 2025, created a temporary federal income tax deduction for the premium portion of FLSA overtime pay. The deduction applies to tax years 2025 through 2028 only. 2025 was a no-penalty transition year. Penalties apply beginning with tax year 2026.

What 'Qualified Overtime' Means

The deduction applies to the premium portion of overtime pay, which is the 'half' in time-and-a-half. If an employee earns $20 per hour and works 10 hours of overtime in a week at $30 per hour, the overtime pay is $300 total. Of that $300, the premium portion is $100 (10 hours x $10, the half-time premium). That $100 is the qualified overtime amount. The deduction is for employees to claim on their individual tax returns, but employers are responsible for tracking and reporting it correctly.

Deduction Limits, Phase-Out, and Sunset Date

The OBBBA overtime deduction has three important limits employers should communicate to their workforce:

-

Cap: $12,500 per return for single filers; $25,000 for joint filers.

-

Phase-out: The deduction begins to reduce for employees with modified adjusted gross income (MAGI) above $150,000, or $300,000 for joint filers.

-

Sunset: The deduction is temporary. It applies only to tax years 2025 through 2028. Unless Congress acts to extend it, the deduction expires after 2028.

Tax Year 2025: Transition Year

The OBBBA took retroactive effect January 1, 2025. However, 2025 was designated a transition year. No penalties were imposed on employers who did not separately report qualified overtime on 2025 W-2s. Employers could voluntarily report in Box 14 or via a separate statement.

Tax Year 2026: Reporting Is Now Required

Beginning with tax year 2026, separate reporting of qualified overtime on W-2 forms is mandatory. The draft 2026 Form W-2 uses Box 12 code 'TT' for qualified overtime compensation. Forms 1099-NEC and 1099-MISC are also updated for non-employee workers. Employers who fail to separately report correctly face penalties of $60 to $660 per W-2 under IRS sections 6721 and 6722.

What Employers Need to Do Now

Confirm that your payroll system is configured to track the premium portion of overtime separately from regular overtime pay. Ask your payroll provider specifically whether Box 12 code 'TT' is enabled for 2026 W-2 reporting. If you are manually processing payroll, establish a tracking method for the premium portion of each nonexempt employee's overtime pay before Q4 W-2 preparation begins.

📌 Critical Note: This deduction only applies to FLSA overtime-eligible nonexempt employees. Exempt employees do not generate qualified overtime compensation regardless of how many hours they work. This is another reason that correct classification matters: it determines not just whether you owe overtime, but how you report compensation on W-2s.

What Happens If You Misclassify an Employee for Overtime?

Overtime misclassification can expose an employer to back wages for up to three years, liquidated damages that double that total, civil penalties, attorney's fees, and in willful cases, criminal prosecution. The DOL's Wage and Hour Division recovers hundreds of millions of dollars in back wages from employers annually. A single misclassified employee who regularly worked five overtime hours per week at $20/hour over three years represents more than $23,000 in back wages alone, before liquidated damages.

Back Wages

The employer owes 100 percent of all unpaid overtime for the period of the violation. The standard lookback period is two years, but for willful violations, it extends to three years.

Liquidated Damages

Under the FLSA, an employer found in violation automatically owes liquidated damages equal to the amount of back wages, unless the employer can demonstrate the violation was made in good faith with a reasonable belief it complied with the law. In practice, this effectively doubles total liability.

Civil Money Penalties and Criminal Exposure

The DOL can levy civil money penalties for willful or repeated violations. For willful violations, employers may also face criminal prosecution, fines up to $10,000, and potential imprisonment on a second conviction.

Attorney's Fees and Court Costs

If an employee files a private lawsuit and prevails, the employer pays the employee's attorney's fees and court costs. Wage and hour attorneys commonly take these cases on contingency, so the practical barrier for employees to file suit is low.

Class and Collective Actions

A single misclassification finding can open the door to a collective action if other employees in similar roles were classified the same way. What starts as one employee's claim can become a company-wide liability affecting dozens or hundreds of current and former workers.

The good news: most misclassification risk is preventable with a documented, role-by-role classification review and accurate job descriptions. The goal is not to find reasons to deny overtime, but to accurately reflect what employees actually do so that any classification can be defended if ever questioned.

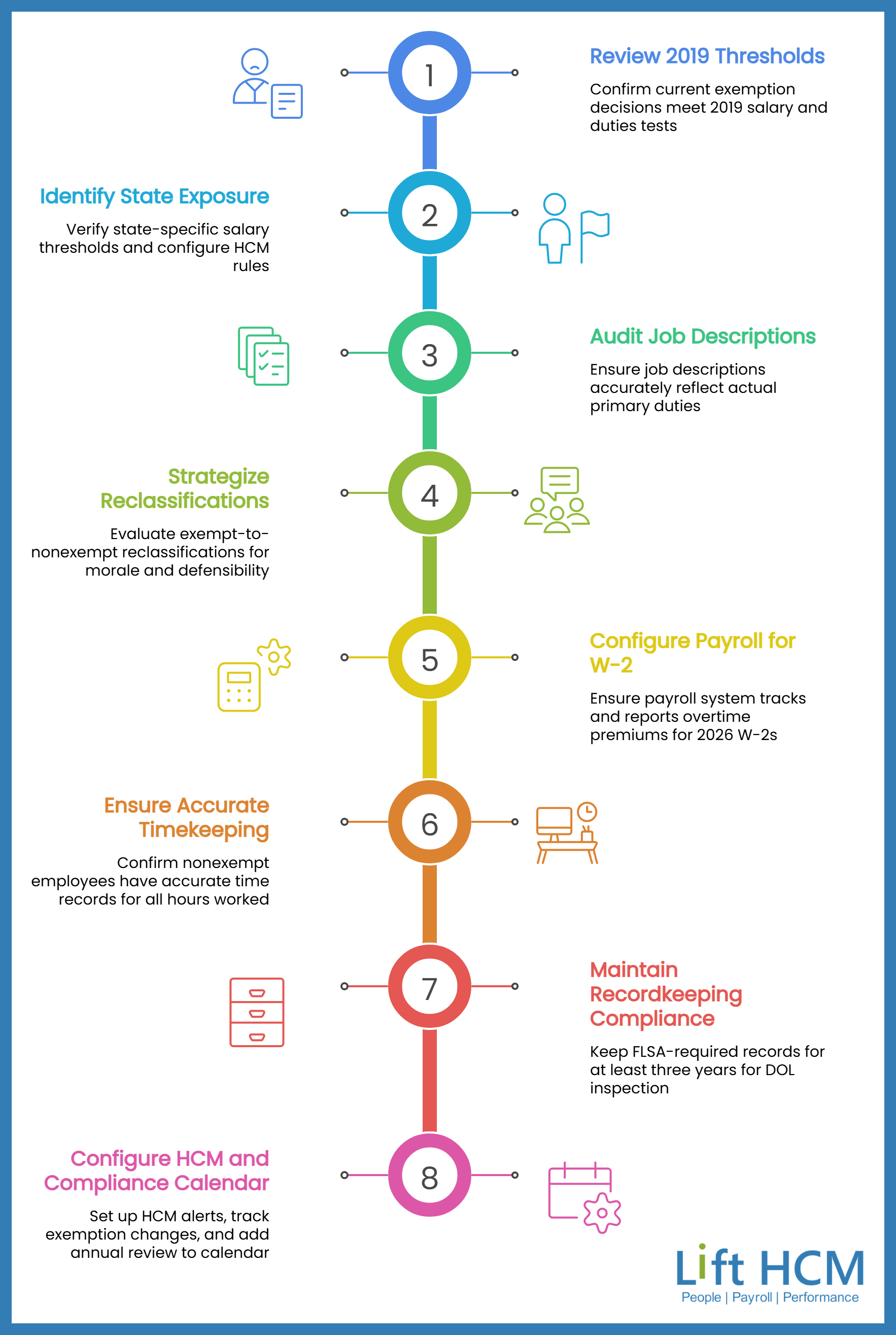

What Should Your Overtime Compliance Action Plan Look Like?

With the federal threshold confirmed at $684/week and OBBBA W-2 reporting now required, employers should complete eight steps: (1) confirm current classifications, (2) identify state exposure, (3) audit job descriptions, (4) address any 2024 reclassifications, (5) configure payroll for Box 12 'TT' reporting, (6) verify timekeeping, (7) establish recordkeeping, and (8) update your HCM system and compliance calendar.

Step 1: Confirm Your Current Classifications Reflect the 2019 Thresholds

If your organization made exemption decisions based on the anticipated 2024 thresholds, review those decisions now. Any employee classified as exempt should meet both the salary level test ($684 per week) and the applicable duties test. Document the basis for each exemption.

Step 2: Identify State-Level Exposure

For every state where you have employees, confirm the applicable salary threshold. This is especially important if you operate in California ($1,352/week), Washington ($1,541.70/week), Colorado ($1,111.23/week), Maine ($871.16/week), or New York (varies by region). Configure jurisdiction-based rules and alerts in your HCM platform.

Step 3: Audit Job Descriptions Against Actual Duties

Exemption status is only as defensible as the accuracy of your documentation. Review job descriptions to confirm they reflect each role's actual primary duties. Pay particular attention to any salaried employees who may have drifted into nonexempt work without a corresponding reclassification.

Step 4: Address Any 2024 Reclassifications Strategically

For employees reclassified from exempt to nonexempt in anticipation of the 2024 rule, evaluate each role individually before making any changes. Consider employee morale and retention, duties test defensibility, state-level requirements, and how the change was originally communicated.

Step 5: Confirm Your Payroll System Is Configured for OBBBA W-2 Reporting

For tax year 2026, your payroll system must separately track and report the premium portion of overtime on W-2 forms using Box 12 code 'TT.' Ask your payroll provider specifically whether this is enabled. If you are manually processing payroll, establish a tracking method for each nonexempt employee's overtime premium now, before Q4 W-2 preparation begins.

Step 6: Ensure Accurate Timekeeping for Nonexempt Employees

Any employee classified as nonexempt must have accurate time records for all hours worked, including remote work. Confirm that your time tracking system captures all compensable time. Managers cannot withhold pay for unapproved overtime, though unapproved overtime can be addressed through coaching and documented policy enforcement.

Step 7: Establish and Maintain Recordkeeping Compliance

The FLSA requires employers to maintain records of hours worked and wages paid for at least three years, in any format, available for DOL inspection. If your business is ever investigated, your records are your primary defense. Courts may accept an employee's estimate of hours worked if the employer has no records to counter it.

Step 8: Configure Your HCM System and Update Your Compliance Calendar

Flag near-threshold salaries for periodic review, set alerts when overtime hours spike, track exemption status changes with effective dates, configure jurisdiction-specific pay rules for multi-state workforces, and generate compliance reports for internal audits. Add an annual exemption review to your HR calendar and subscribe to DOL regulatory updates for advance notice of any future rulemaking.

Frequently Asked Questions About the DOL Overtime Rule in 2026

What Is the Current FLSA Overtime Salary Threshold in 2026?

The current federal threshold is $684 per week ($35,568 per year) for most white-collar exemptions. The DOL announced the technical amendment on May 14, 2026, and published it in the Federal Register on May 15, 2026, confirming the 2019 thresholds and officially rescinding the 2024 rule. The highly compensated employee threshold is $107,432 per year, including at least $684 per week paid on a salary or fee basis.

Was the DOL 2024 Overtime Rule Vacated?

Yes. The 2024 rule was vacated by the U.S. District Court for the Eastern District of Texas in November 2024, followed by a second ruling from the Northern District of Texas. The DOL dropped its appeals on May 5 and May 7, 2026, the Fifth Circuit dismissed both cases, and the DOL published the technical amendment on May 15, 2026, formally removing the 2024 rule from the Code of Federal Regulations.

Do I Have to Reverse Salary Increases or Reclassifications Made for the 2024 Rule?

No. There is no legal requirement to undo changes made in anticipation of the 2024 rule. Salary increases can be maintained, and employees who were reclassified to nonexempt may be eligible for re-exemption if they meet the restored $684 per week threshold and the applicable duties test. Any changes should be evaluated on a role-by-role basis and documented carefully.

What Is a Salaried Nonexempt Employee?

A salaried nonexempt employee is a worker paid a fixed salary who is still legally entitled to overtime pay. This happens when a salaried employee either earns less than $684 per week or earns above that threshold but does not meet the applicable duties test. Being paid a salary does not automatically confer exempt status. Salaried nonexempt employees must have their hours tracked and receive overtime pay for hours over 40 in a workweek.

What Are the Penalties for Overtime Misclassification?

Overtime misclassification can result in back wages for up to two years (three years for willful violations), plus liquidated damages equal to the back wages owed, effectively doubling total liability. The DOL can also impose civil money penalties for willful or repeated violations, and willful violations can result in criminal prosecution and fines up to $10,000. If an employee files a private lawsuit and prevails, the employer is also responsible for attorney's fees and court costs.

What Are the Duties Tests, and Why Do They Matter?

The duties tests define what type of work an employee must primarily perform to qualify as exempt from overtime. There are separate tests for executive, administrative, professional, computer, and outside sales employees. Meeting the salary threshold is necessary but not sufficient: an employee must also pass the applicable duties test, or they are entitled to overtime regardless of their salary.

My Business Operates in Multiple States. Which Overtime Rules Apply?

Federal law sets the floor. When a state sets a higher salary threshold or a narrower duties test, the state standard applies to employees in that location. Employers must comply with whichever standard is most protective of the employee. The operative threshold is based on where the employee physically performs their work, not where the employer is headquartered.

What Does the OBBBA Overtime Deduction Mean for My Payroll Reporting?

Starting with tax year 2026, employers must separately report qualified overtime compensation on W-2 forms using Box 12 code 'TT.' Qualified overtime is the premium portion of FLSA overtime pay (the 'half' in time-and-a-half), capped at $12,500 per return ($25,000 joint), and phases out above $150,000 MAGI. The deduction is temporary: it expires after tax year 2028. The 2025 tax year was a no-penalty transition year. Penalties under IRS sections 6721 and 6722 apply beginning with tax year 2026.

How Long Do I Need to Keep Overtime Records?

The FLSA requires employers to maintain records of hours worked and wages paid for at least three years, in any format, available for DOL inspection. Courts may accept an employee's estimate of hours worked if the employer has no records to counter it, which makes accurate recordkeeping one of the most important defenses an employer has.

Is the Overtime Threshold Going to Change Again Soon?

As of June 2026, no proposed rulemaking on overtime salary thresholds is currently pending, and no automatic adjustment mechanism is in place. The DOL's May 2026 amendment noted that future rulemaking remains possible. Any future change would require a formal notice and comment process, giving employers advance notice before a new threshold takes effect.

Are There Overtime Rules That Differ for Restaurant or Hospitality Workers?

The FLSA's white-collar exemption thresholds apply across industries. However, the tipped minimum wage, tip credit rules, and the Section 7(i) commissioned-employee overtime exemption add significant complexity for restaurant and hospitality employers. The DOL issued a clarifying opinion letter in January 2026 (FLSA 2026-4) addressing how service charges and tips are treated under Section 7(i), which is directly relevant for hospitality operators who rely on mandatory service charge models.

Get the Right Overtime Compliance Foundation for Your Business

For two years, employers navigated some of the most disruptive FLSA overtime rulemaking in recent memory. The 2024 rule's proposed increases, the court battles, the ongoing uncertainty about which threshold actually applied, and the addition of a new W-2 reporting requirement all hit at once. Making compliance decisions in that environment was genuinely hard.

Now, the picture is clear. The DOL's May 14-15, 2026 technical amendment formally confirms $684 per week as the operative federal threshold, the automatic adjustment mechanism is gone, the 2024 rule is officially off the books, and the OBBBA W-2 reporting requirements are in effect for tax year 2026.

With the right payroll and HCM infrastructure in place, you can stop reacting to regulatory changes and start managing compliance proactively. At Lift HCM, we help small and mid-sized businesses build that foundation: accurate classification tracking, multi-state pay rule configuration, timekeeping that captures every compensable hour, OBBBA-ready overtime reporting using Box 12 code 'TT,' and a team that keeps you current as the rules evolve. Contact our team to talk through your situation and get a compliance plan built for your workforce.

Content in this article reflects publicly available DOL, IRS, and state agency guidance as of June 2026.

Topics:

.png?width=1536&height=1024&name=Create%20a%20background%20that%20reads%2c%20How%20Long%20to%20Keep%20P%20(1).png)

{kind=link}