The landscape of employer tax compliance is shifting for 2026, but not in the way many originally feared.

While the expiration of the 2017 Tax Cuts and Jobs Act (TCJA) was predicted to cause a major tax law reversion, recent legislation has made many key provisions permanent. This eliminates the threat of significantly higher tax rates, but introduces a new compliance focus on managing numerous inflationary adjustments and implementing valuable new employee benefits.

At Lift HCM, we've guided organizations through every major regulatory change. We understand that accurate information and proactive system preparation are the keys to avoiding costly surprises.

In this article, we'll confirm the permanent tax provisions, detail the critical new benefit limits (like the enhanced Dependent Care FSA), and provide a clear roadmap for preparing your payroll and workforce management processes for 2026.

Table of Contents

- What Changes Are Actually Happening in 2026?

- Critical New and Adjusted Employee Benefits for 2026

- Common Mistakes Employers Must Avoid in 2026

- 5-Step Plan to Prepare Your Payroll and Benefits for 2026 Tax Law Changes

- Frequently Asked Questions About 2026 Tax Changes and Employee Benefits

- Beyond Compliance: Turning 2026 Changes into an Advantage

What Changes Are Actually Happening in 2026?

The biggest news for employers is one of stabilization: most major individual tax elements set to "sunset" have been made permanent. The primary compliance focus has shifted from structural tax code changes to managing inflation-based limits and new benefit structures.

| Area of Impact | TCJA Rule (2018-2025) | ACTUAL 2026 STATUS (Permanent) | Employer Impact & Action |

| Individual Tax Brackets | Lowered across most income levels (7 rates). | Permanent: Current seven tax rates (10% to 37%) remain permanent. Brackets are adjusted for inflation. | Action: Mandates new payroll withholding tables for 2026 (reflecting inflation-adjusted brackets). Rates themselves are stable. |

| Standard Deduction | Doubled from pre-TCJA law. | Permanent: The higher deduction amounts are permanent, increasing to approximately $32,200 MFJ for 2026. | Action: Update payroll systems with the new 2026 inflation-adjusted figures. |

| Personal Exemptions | Suspended/Set to $0. | Permanent: The suspension of the personal exemption is permanent. | Impact: No change. Payroll systems will continue to ignore personal exemptions. |

| Moving Expenses | Employer reimbursements are Taxable (except for military). | Permanent: Taxability for non-military employees was made permanent. | Action: Continue treating non-military reimbursements as Taxable Wages subject to withholding and FICA. |

| Employee Business Expenses | Most unreimbursed expenses are Eliminated as a deduction. | Permanent: The elimination of these deductions was made permanent. | Impact: No change to payroll, as employees still cannot deduct these expenses. |

| Fringe Benefit Deduction | Employer deduction for Qualified Transportation Fringe is Eliminated. | Permanent: The elimination of the employer deduction for these benefits remains permanent. | Action: No change to how employers deduct the cost of these benefits. |

Critical New and Adjusted Employee Benefits for 2026

The true compliance and strategic challenge for 2026 lies in the permanent status of certain benefits and the annual inflation increases. HR and payroll teams must focus on these areas immediately.

1. Dependent Care FSA: Major New Limit

Effective January 1, 2026, the annual maximum contribution for Dependent Care Flexible Spending Accounts (DCFSAs) is permanently increased from $5,000 to $7,500 ($3,750 for married filing separately).

This long-awaited increase is a major benefit for employees but creates three key compliance considerations for employers:

- Plan Amendments: Employers must actively amend their plan documents to adopt the new $7,500 limit. This is not an automatic change.

- Non-Discrimination Testing (NDT): The increased limit could make it harder for some employers to pass the 55% Average Benefits Test, which ensures benefits do not unfairly favor Highly Compensated Employees (HCEs).

- Employee Communication: Employees must be informed of the new limit during open enrollment to make accurate 2026 elections.

2. Student Loan Repayment Assistance is Permanent

The tax-free exclusion for employer-provided payments toward an employee's student loans (up to $5,250 annually) was scheduled to expire. Recent legislation has made this provision permanent.

- Action: Employers should continue offering this program as a non-taxable benefit and ensure plan documents reflect the permanent status. This is a powerful, compliant recruitment tool.

3. Key Inflationary Adjustments (COLA)

Payroll systems must be updated to reflect the 2026 inflation adjustments, which impact numerous plan limits.

| Benefit/Limit | 2025 Limit (Approx.) | 2026 Limit (Confirmed) | Payroll Action Required |

| Health FSA Max Contribution | $3,300 | $3,400 | Update maximum election amounts in cafeteria plans. |

| Qualified Transportation Fringe | $325/month | $340/month | Update pre-tax deduction limits in payroll/benefit systems. |

| 401(k) Employee Elective Deferral | $23,500 | $24,500 | Update retirement deferral limits in payroll and plan documents. |

| HSA Max Contribution (Self-Only) | $4,300 | $4,400 | Update contribution limits for HSA-eligible employees. |

| Tax-Exempt Adoption Assistance | $17,280 | $17,670 | Update maximum exclusion amount in payroll and benefits administration. |

BONUS: IRS Tax Withholding Estimator Tool

Common Mistakes Employers Must Avoid in 2026

The focus is no longer on if the law will change, but on how quickly and accurately you manage the compliance requirements for these permanent rules.

- Mistake #1: Assuming Benefits Are Automatic. Critical: The new $7,500 Dependent Care FSA (DCFSA) limit requires a plan amendment. Without this, your plan remains at the old $5,000 limit.

- Mistake #2: Ignoring Non-Discrimination Testing. The higher DCFSA limit makes NDT more challenging. Employers must consider running interim testing early in 2026 and adjusting HCE (Highly Compensated Employees) elections if necessary to prevent HCE benefits from becoming taxable.

- Mistake #3: Assuming Payroll Software Handles Everything. While vendors update tax tables, the specific implementation of new benefit limits and updated W-4 information relies heavily on HR oversight and system testing.

- Mistake #4: Delaying W-4 Updates. New W-4 guidance will reflect the permanent tax brackets and the inflation-adjusted standard deduction. Employees must be encouraged to file updated W-4s for accurate withholding in January 2026.

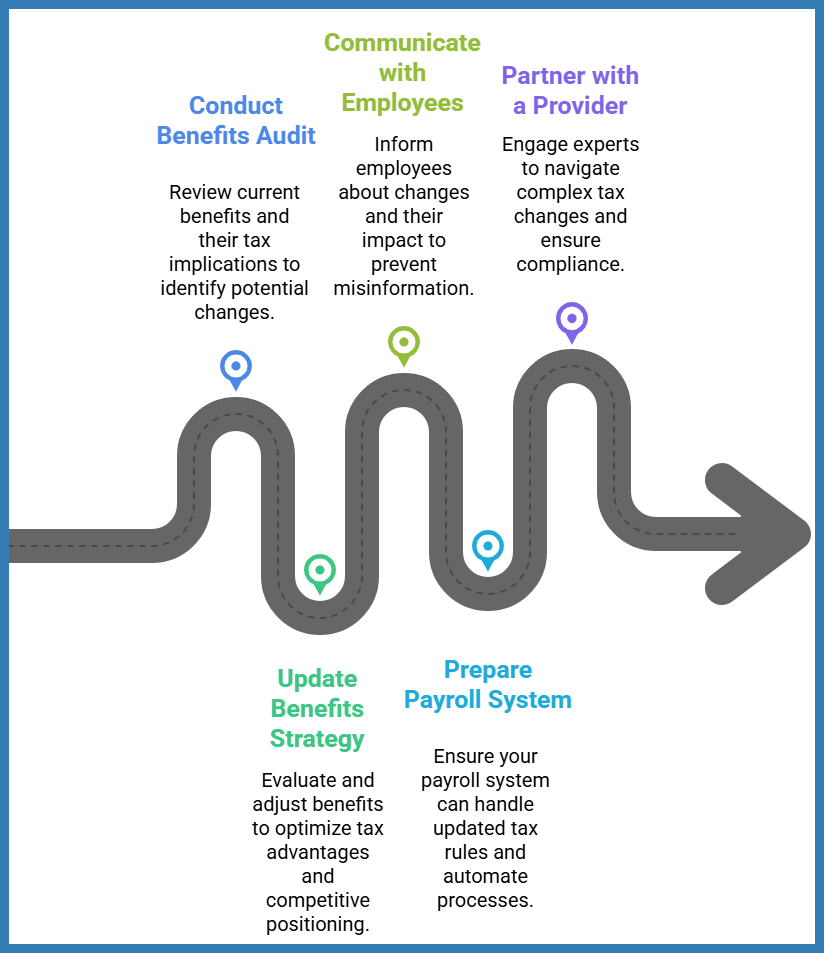

5-Step Plan to Prepare Your Payroll and Benefits for 2026 Tax Law Changes

Preparation is the key to avoiding stress and last-minute problems. Here's your action plan for navigating the 2026 tax changes employee benefits will endure:

Frequently Asked Questions About 2026 Tax Changes and Employee Benefits

Q: What tax laws are changing in 2026? A: Many provisions of the Tax Cuts and Jobs Act (TCJA) expire on December 31, 2025. Unless Congress acts, the rules revert to pre-2017 levels in 2026. Key areas affecting employers include fringe benefit taxation, moving expense treatment, and various employer deductions.

Q: Will employee benefits become more expensive in 2026? A: Not all benefits will be affected by the 2026 tax changes. Benefits tied to TCJA provisions—such as certain fringe benefits, moving expense reimbursements, and meal deductions—may see tax treatment changes that affect employer costs. The financial impact depends on your specific benefits portfolio.

Q: Do employers need to update payroll systems for 2026 tax changes? A: Yes. Employers should expect new IRS withholding tables, updated W-4 guidance, and adjustments to how certain benefits appear on W-2 forms. Payroll systems need to be configured and tested to handle these changes before January 1, 2026. Waiting until late December creates unnecessary risk of payroll errors.

Q: When will the IRS release final guidance on 2026 tax changes? A: The IRS typically releases updated withholding tables and detailed guidance close to year-end, often in November or December. However, preliminary guidance may come earlier based on Congressional activity. Employers should have begun to prepare in mid-2025 rather than waiting for final IRS publications.

Q: How can small businesses prepare for 2026 tax changes? A: Start by conducting a benefits audit to identify affected benefits. Review your payroll system capabilities and timeline for implementing updates. Communicate early with employees about potential changes. Consider partnering with a compliance-focused payroll provider that can handle the technical compliance work.

Beyond Compliance: Turning 2026 Changes into an Advantage

Tax law changes have created stress and confusion for employers for years. The upcoming 2026 changes can feel overwhelming, especially when they affect payroll, benefits, compliance, and employee communication.

You now understand what the 2026 tax law changes are, how they may affect employee benefits, what mistakes to avoid, how to estimate potential impacts, and how to prepare your HR and payroll processes with confidence.

With the right support — and with tools designed to keep you compliant through shifting tax rules — you can move into 2026 fully prepared. At Lift HCM, we help organizations transition smoothly through tax and benefit rule changes with accurate payroll, integrated benefits, and hands-on support from real experts.

Topics:

.jpg?width=4000&height=3723&name=stack-papers-tax-concept-illustration(1).jpg)

.jpeg?width=1344&height=768&name=two%20binders%20stacked%20on%20top%20of%20eachother%20on%20top%20of%20paperwork%20and%20a%20calculator(1).jpeg)

.jpeg?width=1792&height=1024&name=glass%20jar%20on%20a%20restaurant%20table%20top%20bar%20with%20someone%20putting%20cash%20tips%20in%20it(1).jpeg)

.jpeg?width=1792&height=1024&name=a%20restaurant%20employee%20counting%20cash%20tips%20at%20a%20table(1).jpeg)

.jpg?width=5000&height=3337&name=account-assets-audit-bank-bookkeeping-finance-concept(1).jpg)

{kind=link}