This article is for informational purposes only and does not constitute legal or tax advice. Confirm current requirements with the IRS, your state labor or tax department, or qualified legal counsel before making filing decisions.

ACA reporting catches a lot of employers off guard. The form requires data you need to be capturing all year long, the deadlines cluster into a narrow window early in the year, and the codes on Lines 14 and 16 can feel like a foreign language if you haven't filled them out before.

For Applicable Large Employers (businesses with 50 or more full-time and full-time equivalent employees), Form 1095-C is not optional. Filing late, filing incorrectly, or failing to make the form available to employees can result in significant IRS penalties that compound quickly at $340 per return.

At Lift HCM, we work with HR and benefits administrators every day who are managing ACA obligations alongside everything else on their plates. We understand the pressure of getting this right, and the consequences of getting it wrong. Our goal with this guide is to give you a clear, honest look at exactly what Form 1095-C requires so you can walk into any filing season prepared, not scrambling.

This article walks you through exactly what Form 1095-C is, who must file it, what each section requires, and the deadline calendar you can plan around every year. By the end, you'll know whether your current data collection is capturing what the IRS actually needs, and where a payroll platform like isolved makes the whole process significantly easier.

Table of Contents

What Is IRS Form 1095-C?

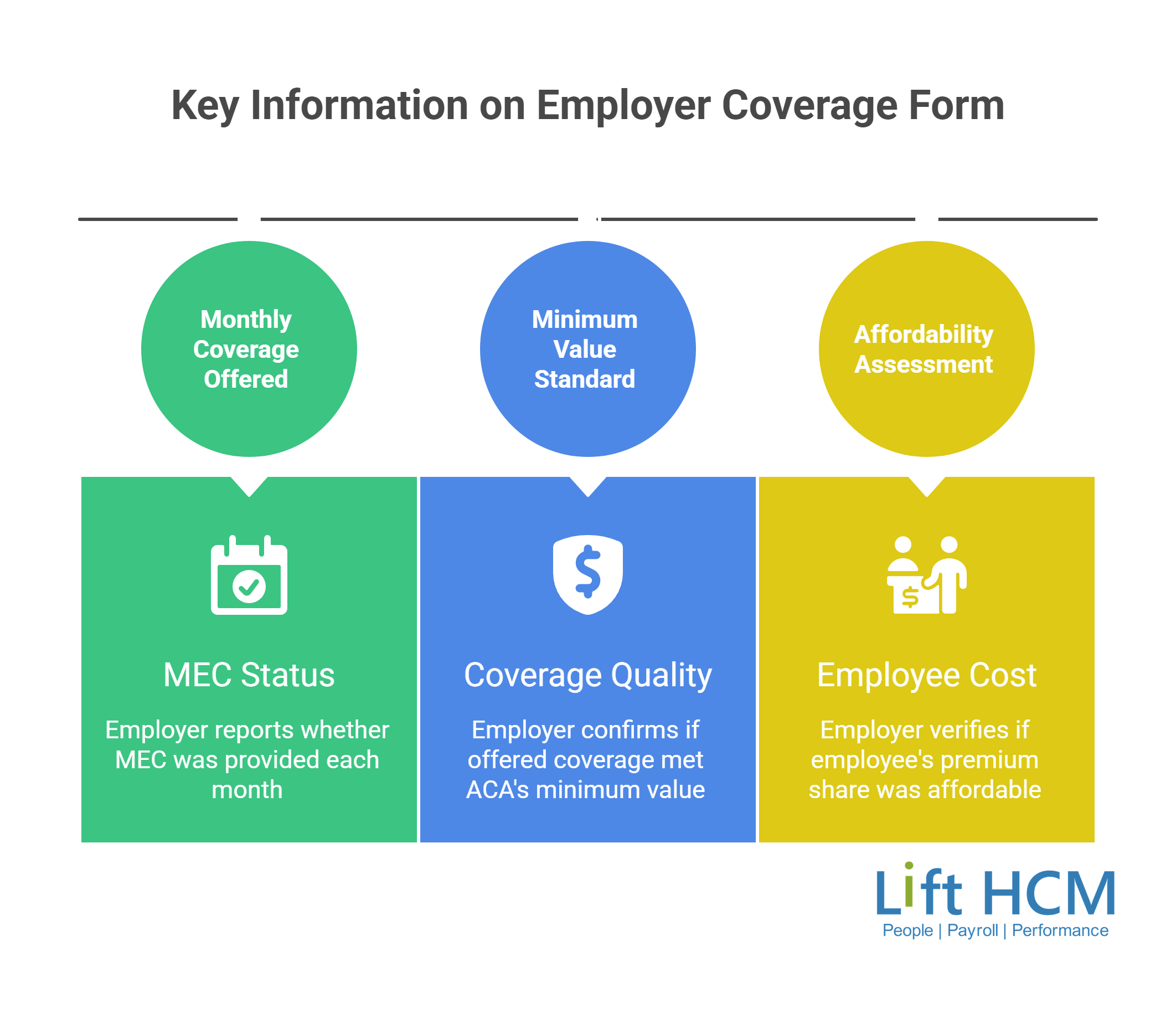

Form 1095-C is an information return used by Applicable Large Employers (ALEs) to report health coverage offers made to full-time employees. The IRS uses it to enforce the ACA's employer shared responsibility provisions, also known as the employer mandate.

The form tells the IRS three things:

- Whether the employer offered minimum essential coverage (MEC) to the employee each month

- Whether the coverage offered met the ACA's minimum value standard (covering at least 60% of the plan's total cost)

- Whether the coverage was affordable, meaning the employee's share of the lowest-cost self-only premium didn't exceed a set percentage of household income

Form 1095-C is filed in tandem with Form 1094-C, which is the transmittal form that summarizes all 1095-C returns for the IRS. Think of 1094-C as the cover sheet and 1095-C as the individual employee-level detail.

Form 1095-C: Filed for each full-time employee. Reports the offer of coverage (or lack thereof) for each of the 12 months of the calendar year. One form per employee. Copies go to both the IRS and the employee (or are made available on request).

Form 1094-C: The transmittal cover form submitted once per employer to accompany all 1095-C returns. Only one 1094-C should be designated as the Authoritative Transmittal. Reports aggregate employer-level data including total full-time employee counts and ALE membership.

Who Is Required to File Form 1095-C?

Only Applicable Large Employers (ALEs) are required to file Form 1095-C. The IRS defines an ALE as an employer that employed an average of 50 or more full-time employees, including full-time equivalents (FTEs), during the prior calendar year.

To determine your ALE status for 2025 (which affects your 2026 filing obligation):

- Count full-time employees: Those who averaged 30 or more hours of service per week, or 130 or more hours per month

- Calculate FTEs: Add all hours worked by part-time employees in a month, divide by 120

- Add full-time count plus FTE count for each month, then average across all 12 months

- If the result is 50 or more, you are an ALE for the following year

FTE Calculation Example: You have 40 full-time employees working 30+ hours/week, plus 20 part-time employees who each work 80 hours/month. Part-time FTEs = (20 × 80) ÷ 120 = 13.3 FTEs. Total = 40 + 13.3 = 53.3, rounded down to 53. You are an ALE and must file Form 1095-C for each of your 40 full-time employees.

Form 1095-C must be filed for every employee who was full-time for at least one month during the calendar year, even if they left the company mid-year, even if they declined coverage, and even if they enrolled in a spouse's plan instead.

What Are the 2026 ACA Reporting Deadlines?

ACA reporting runs on a predictable annual cadence, so you can plan around it. The dates below apply to the 2025 tax year (the coverage offered and months of enrollment during calendar year 2025), but the same rhythm repeats every year: employee statements and paper filing at the start of March, electronic filing at the end of March, and the PCORI fee at the end of July. Save this section as your recurring calendar.

⏰ Due next: the July 31 PCORI fee. If you sponsor a self-insured or level-funded medical plan (including certain HRAs), your PCORI fee for a plan year that ended in 2025 is due July 31, 2026, filed on IRS Form 720. For calendar-year plans, the rate is $3.84 per covered life. This is the one 2025-cycle deadline still open, so if it applies to you, it is the item to handle now. The employee statement and IRS filing deadlines for the 2025 tax year (early to late March) have already passed; the same deadlines return for the 2026 tax year in early 2026.

Here are the key dates for the full 2025 reporting cycle:

|

Deadline |

Requirement |

Notes |

|---|---|---|

|

March 2, 2026 |

Furnish 1095-C to employees OR post website notice of availability |

The automatic 30-day extension of the January 31 furnishing deadline lands on March 2, 2026. No further extension is available. |

|

March 2, 2026 |

IRS paper filing deadline (for 1094-C + 1095-C) |

Paper filing only permitted if you file fewer than 10 total information returns. Most ALEs must e-file. |

|

March 31, 2026 |

IRS electronic filing deadline (for 1094-C + 1095-C) |

Required for any employer filing 10 or more information returns in aggregate (including W-2s, 1099s, and 1095-Cs combined). |

|

July 31, 2026 |

PCORI fee due (self-insured plan sponsors) |

For plan years ending January 1 through September 30, 2025: $3.47 per covered life. For plan years ending October 1 through December 31, 2025 (including calendar-year plans): $3.84 per covered life. |

🆕 New in 2026: Alternative Furnishing Method Effective for the 2025 tax year (filed in 2026), and thanks to recent federal legislation (the Paperwork Burden Reduction Act and the Employer Reporting Improvement Act, both signed in December 2024), ALEs no longer need to automatically mail Form 1095-C to every full-time employee. You may instead post a clear, conspicuous notice on your company's benefits website by March 2, 2026. The notice must remain posted through October 15, 2026, must be reasonably accessible to all affected employees, and must include an email address, a physical address, and a phone number employees can use to request their form or ask questions. If an employee requests the form, you must provide it within 30 days of the request (or by January 31, whichever is later).

What Is the ACA Affordability Threshold for 2026?

The ACA affordability rate for the 2026 plan year increases to 9.96%, up from 9.02% for 2025. This is the maximum percentage of household income that an employee can be required to pay for the lowest-cost self-only plan offered by their employer.

If your self-only premium contribution exceeds 9.96% of an employee's household income, the coverage is considered unaffordable, and you may face an employer shared responsibility penalty if that employee receives a premium tax credit through the marketplace.

Because you typically don't know employees' household incomes, the IRS provides three safe harbor methods to determine affordability:

- W-2 Wages Safe Harbor: The employee's premium contribution does not exceed 9.96% of their Box 1 W-2 wages

- Rate of Pay Safe Harbor: The monthly premium doesn't exceed 9.96% of 130 hours times the employee's hourly rate (or monthly salary for exempt staff)

- Federal Poverty Level (FPL) Safe Harbor: The monthly self-only premium doesn't exceed 9.96% of the federal poverty level for a single individual divided by 12

📊 Affordability Reference: The 2026 Plan Year ACA affordability threshold is 9.96% (a significant jump from 9.02% in 2025). Your maximum monthly employee contribution under the FPL safe harbor depends on when your plan year begins:

Calendar-Year Plans (Beginning Jan 1, 2026): May look back to the 2025 FPL ($15,650). The maximum monthly self-only premium is strictly $129.90 ($15,650 × 9.96% ÷ 12).

Non-Calendar-Year Plans (Beginning later in 2026): May utilize the finalized 2026 FPL ($15,960). This increases the maximum allowable monthly premium to $132.47 ($15,960 × 9.96% ÷ 12).

Note: These specific figures apply to the 48 contiguous states and D.C. Higher thresholds apply in Alaska and Hawaii.

How Do You Fill Out Form 1095-C? Section by Section

Part I: Employee and Employer Information

Part I is straightforward. You'll enter the employee's name, Social Security Number (SSN), and address. You may truncate the SSN to the last four digits on copies furnished to employees (but not on copies filed with the IRS). You'll also enter the employer's full legal name and EIN.

Part II: Employee Offer of Coverage (Lines 14 to 16)

Part II is the most complex and most commonly misunderstood section. You'll complete Lines 14, 15, and 16 for each calendar month. If the same information applies for all 12 months, you can enter it in the "All 12 Months" column.

|

Line |

Field |

What It Reports |

|---|---|---|

|

Line 14 |

Offer of Coverage Code |

A two-digit code (1A through 1U) indicating what coverage was offered and to whom. Common codes: 1A = Qualifying offer (MEC, minimum value, affordable using FPL safe harbor, offered to employee and family); 1E = MEC with minimum value offered to employee, spouse, and dependents; 1H = No offer made. |

|

Line 15 |

Employee Required Contribution |

The monthly dollar amount the employee must pay for the lowest-cost self-only plan. Only complete Line 15 when certain Line 14 codes are used (1B, 1C, 1D, 1E, 1J, 1K, and others). Leave blank if you used code 1A. |

|

Line 16 |

Applicable Section 4980H Safe Harbor |

A two-digit code (2A through 2I) indicating why an employer may not owe a shared responsibility payment for a given month. Common codes: 2C = Employee enrolled in coverage offered; 2D = Employee in a limited non-assessment period (for example, a waiting period or initial measurement period); 2A = Employee not employed during the month. |

Part III: Covered Individuals (Self-Insured Plans Only)

Part III is only required for employers who sponsor a self-insured (or level-funded) health plan. You'll list the name, TIN (or date of birth if TIN unavailable), and covered months for every individual covered by your plan, including employees' dependents.

Does Your Business Need to E-File?

Almost certainly yes. The IRS strictly enforces an electronic filing mandate for any employer filing 10 or more information returns in aggregate. This threshold is calculated using an aggregate counting method, meaning you cannot look at your forms in isolation. To determine your filing requirement, you must add together almost all information returns your business files across the calendar year—including Forms W-2, 1099 series, 1094-C, and 1095-C.

Because virtually all Applicable Large Employers (ALEs) file W-2s and 1099s in addition to their required 1095-Cs, almost every ALE automatically crosses this 10-return threshold. Paper filing is entirely unavailable unless you are an exceptionally small business with minimal filings across all return types.

All electronic submissions must be transmitted securely through the official IRS Affordable Care Act Information Returns (AIR) system. Most ALEs utilize a trusted payroll provider, benefits administrator, or specialized third-party compliance software to handle this electronic formatting and submission automatically.

Which States Require Separate ACA Reporting?

In addition to the federal IRS filing, five jurisdictions require employers to file ACA-related forms directly with the state. If you have even one employee residing in any of these states, you must comply with that state's ACA reporting requirements:

- California: Report to the Franchise Tax Board (FTB) by March 31, 2026

- Massachusetts: Report to the Massachusetts Health Connector (Massachusetts uses its own Form MA 1099-HC rather than the federal 1095-C)

- New Jersey: Report to the New Jersey Division of Taxation by March 31, 2026

- Rhode Island: Report to the Rhode Island Division of Taxation by March 31, 2026

- Washington, D.C.: Report to the D.C. Office of Tax and Revenue (generally 30 days after the federal deadline, around April 30, 2026)

Note: Vermont has a state individual mandate but does not currently impose a separate employer reporting requirement, which is why it is not on this list.

⚠️ Multi-State Employer Warning: State ACA filing deadlines generally mirror the federal March 31 electronic filing deadline, but can vary by jurisdiction. Some states accept the federal 1095-C as satisfying the state requirement; others (such as Massachusetts) require separate forms or different fields. Several states, including California, New Jersey, and Rhode Island, maintain their own furnishing rules and may not adopt the federal alternative-notice method. Multi-state employers should verify each state's current requirements annually.

What Are the Penalties for Non-Compliance?

The IRS imposes separate penalties for failure to file with the IRS and failure to furnish to employees. Penalties are adjusted for inflation annually. For the 2026 filing year (covering 2025 returns):

- Failure to file with the IRS: Up to $340 per return, with an annual cap that varies based on business size

- Failure to furnish to employees: Up to $340 per return, separate from IRS filing penalties

- Intentional disregard: No cap applies. Penalties can reach $680 per return or higher.

- Incorrect or incomplete filing: Penalties apply per return even if you file on time

Penalties may be reduced if you correct the failure promptly (for example, a lower per-return amount applies for corrections made within 30 days of the due date), and they may be waived entirely if the failure was due to reasonable cause and not willful neglect.

A business with 75 full-time employees that fails to file any 1095-C returns could face penalties exceeding $51,000 (failure to file plus failure to furnish, at $340 per return each), before any employer shared responsibility payment for failing to offer coverage.

The Bottom Line on Form 1095-C

ACA reporting is one of the most data-intensive compliance obligations Applicable Large Employers face each year. The key to getting it right is collecting the right data throughout the year, not scrambling in February, and using a payroll and benefits platform that tracks offers of coverage, employee premium contributions, and full-time status month by month.

Lift HCM uses isolved's integrated payroll and benefits administration platform to help ALEs track and report this data accurately. When your HR, payroll, and benefits data live in one system, ACA reporting becomes a process rather than a fire drill.

Need help with ACA reporting and 1095-C compliance? Contact Lift HCM. Our team can help you evaluate whether your current payroll setup is capturing the data you need for a clean, penalty-free filing.

Topics:

{kind=link}